SMM Alumina Morning Comment on July 2

Futures Market: Overnight, the most-traded alumina 2509 futures contract opened at 2,948 yuan/mt, with a high of 2,954 yuan/mt, a low of 2,931 yuan/mt, and closed at 2,942 yuan/mt, up 12 yuan/mt or 0.41% from the previous close, with an open interest of 285,000 lots.

Ore Market: Recently, the bauxite market has been relatively quiet, with no significant changes observed in new bauxite transactions or quoted prices. As of July 1, the SMM imported bauxite index stood at $74.21/mt, unchanged from the previous trading day. The SMM Guinea bauxite CIF average price was $74/mt, unchanged from the previous trading day. The SMM Australia low-temperature bauxite CIF average price was $70/mt, unchanged from the previous trading day. The SMM Australia high-temperature bauxite CIF average price was $61/mt, unchanged from the previous trading day.

Industry News:

- Vietnam's bauxite industry chain has finally formed a closed loop, with the Dong Nai aluminum smelter filling the gap in aluminum production projects. Designed with an annual production capacity of 450,000 mt of aluminum, it will purchase the entire output of the Ninh Kieu alumina refinery and the Ninh Kieu alumina refinery in Lam Dong province, addressing the aluminum semis import gap, creating high-paying jobs, and contributing $900 million to GDP annually.

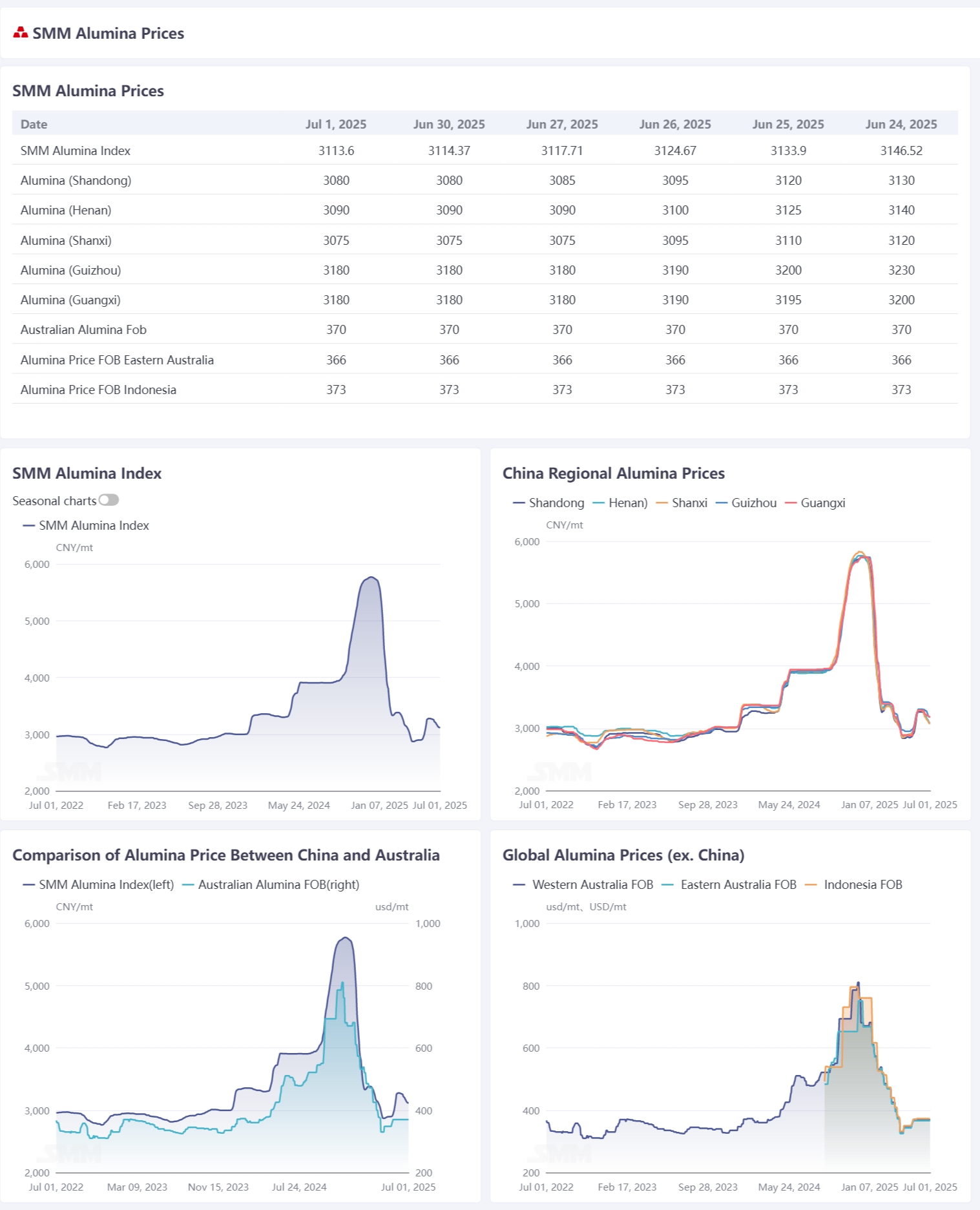

Basis Report: According to SMM data, on July 1, the SMM alumina index had a premium of 186.6 yuan/mt against the latest transaction price of the most-traded contract at 11:30 a.m.

Warrant Report: On July 1, the total registered alumina warrant volume decreased by 8,404 mt from the previous trading day to 21,900 mt. The total registered alumina warrant volume in Shandong remained unchanged at 0 from the previous trading day. The total registered alumina warrant volume in Henan remained unchanged at 0 from the previous trading day. The total registered alumina warrant volume in Guangxi increased by 1,201 mt from the previous trading day to 3,902 mt. The total registered alumina warrant volume in Gansu remained unchanged at 0 from the previous trading day. The total registered alumina warrant volume in Xinjiang decreased by 9,605 mt from the previous trading day to 18,000 mt.

Overseas Market: As of July 1, 2025, the FOB Western Australia alumina price was $370/mt, with an ocean freight rate of $21.9/mt. The USD/CNY selling rate was around 7.18. This price translates to an external selling price of approximately 3,260 yuan/mt at major domestic ports, which is 146 yuan/mt higher than the domestic alumina price. The alumina import window remains closed.

Summary: In the short term, the operating capacity of alumina is expected to remain high, and the spot market supply is expected to remain relatively loose, exerting downward pressure on the alumina spot price. The rise in alumina futures prices in the previous trading days has led to some transfer to delivery warehouse demand, temporarily tightening the alumina spot supply and causing supplier quotes to rebound, halting the decline in spot prices. However, with the recent pullback in alumina futures prices, the risk-free arbitrage profit between futures and spot has turned negative again, and the transfer to delivery warehouse demand may weaken. On the cost side, long-term contract prices for bauxite in Q3 are expected to remain stable or decline primarily. Overall, alumina production costs are anticipated to remain stable or decrease slightly. As alumina prices continue to decline, the cost support effect is expected to gradually come into play. In the short term, spot alumina prices are expected to fluctuate mainly.

[The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make prudent decisions and not rely on this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]